A completely accurate client analytics account is few and far between.

That forces you, brave agency veteran, to roll up your sleeves and try to make sense of the chaos you're looking at for each unique scenario.

You didn't plan for it. You didn't charge for it. And now, if you don't fix it, you'll face an uphill battle in trying to prove the resulted you delivered.

Like it or not, addressing this issue head-on and fixing client analytics can help you sell more, and sell more profitable work.

Here's why.

The Problem with Pricing Digital Services

Most clients have no idea what we do.

They pay us – very well in some cases – despite not truly grasping how we're going to deliver the goods for them.

Sure, they might grock the buzzwords a little bit. They understand the jargon and the high level perspective. But it's mostly a superficial understanding.

When you get down in the weeds, and start describing how exactly to get from A -> B, you start to lose them a little as glazed over eyes stare back at you.

That's not a knock; it's just reality.

In the same way you probably could care less about what's wrong with your car engine and how a mechanic is going to fix it. You just want to know if you're going to be able to make it to Happy Hour in time this afternoon.

More often than not, clients are paying us based on trust. Or a leap of faith. Or our smiles and fashionable clothes.

And when they don't fully grasp the full context of their problem, or the work involved in each painstaking individual step you have to take to fix it, they gravitate towards the one thing that's easy to separate you from everyone else that says they do exactly what you do: price.

Cue competitive bids and escalating downward pricing pressure.

So what do you do the next time around?

You piece together a meager cost plus estimate that rarely includes Profit (and you've undoubtedly underestimated Project Management), double check the marketplace, and rush it out the door.

In contrast, the best, most profitable agencies use value-based pricing. Instead of starting with what their internal costs might be, they start with forecasting:

- The new revenue a client can generate, or

- The cost savings a client might see as a result of working with them.

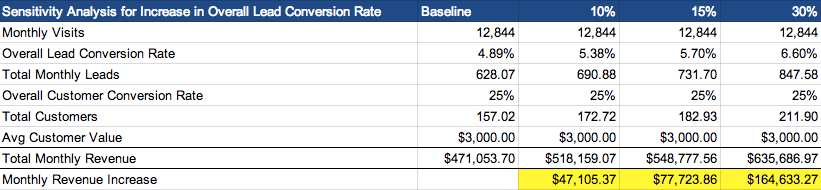

For example, you can take a look at their historical averages of traffic and leads. If you're able to come in and bump that conversion rate by 10%, 15%, or even 30% over the course of a few months, what does that look like in new revenue based on their average customer value?

Boom. If simple conversion tweaks and changes can lead to $40K-$160K+ in new revenue, there's MORE than enough room to pay you 20-30% of that.

That covers your software, payroll, meetings, and then some. You can actually scale a business on that.

Even better, is if you can show how increases in results – less your agency costs – results in NET gains too.

But there's a problem.

You can't even begin to forecast potential revenue for clients like this when they're missing a critical piece of the puzzle.

Why Fixing Your Client's Analytics Should be Priority #1

Value-based pricing includes showing a client the outcome and end results of your work in clear-cut business objectives that they can understand (like leads gained or costs saved).

But…

If they don't have a complete view of their marketing and sales funnel – which, like 97.75% of companies are guilty of – you've got a problem.

To make matters worse, these issues can be tough to spot ahead of time, before you dive into their account (which means you probably didn't plan for it in your timeline and you sure as hell didn't charge for it as a line item).

Maybe the conversion-tracking pixel is on the wrong page (or even worse, sitewide). Or perhaps they're using legacy CRM software that doesn't allow you to figure out what happens after someone becomes a lead (like, where's da revenue coming from?!).

Either way, before you even touch a single line of code, fix a broken link, or put together a wireframe, you need to get an accurate benchmark of where a company is at right now.

Here are three reasons why.

Reason #1. Determine Where Results are Currently Coming From

A quick view of a company's Acquisition Channel performance in Google Analytics can give you a snapshot of where they're at, and how they're doing.

Sure, the visits or sessions piece is moderately helpful, cluing you into which campaigns are delivering (or not).

But the real value comes in analyzing which channels specifically are driving leads and customers (and how much each is worth).

Now you start crossing over from raw data to insight. You're able to draw lines between where budget is being spent and where results are coming from.

This helps you figure out what's already working for clients so you can pour on more, and spot what's already been tried that hasn't worked (so you don't make the same mistakes).

Arguably more important though, is that it will provide you with a baseline to compare against after you deliver your services.

Reason #2. Isolate Campaign/Promotion Attribution

You hear that?

The screeching tires. The scent of burning rubber. A loud crash.

That catastrophic train wreck of epic proportions you're about to witness is your new client's analytics.

Their complex, multi-faceted business has taken its toll, with independent systems for each department that don't work well together (and would require a quant-jock, Business Intelligence analyst to figure out).

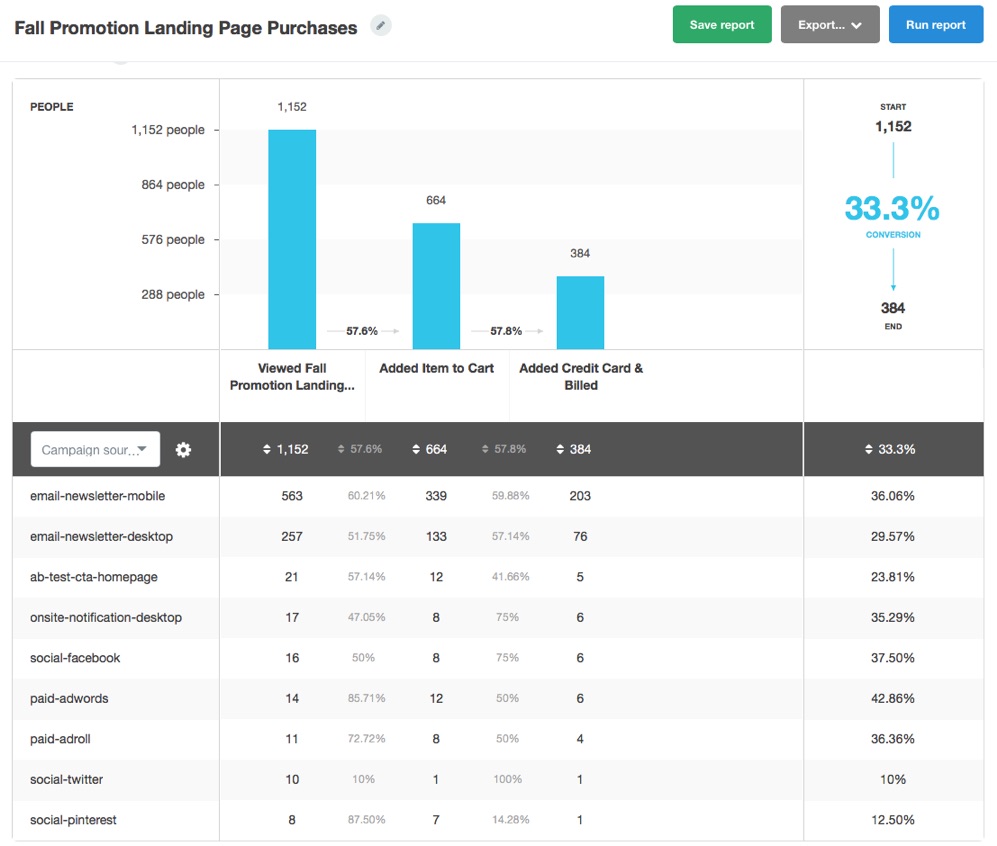

Instead of relying or messing with existing systems, setting up a third-party analytics solution to isolate how your campaign and promotion is performing might be an easy way to sidestep the nightmare.

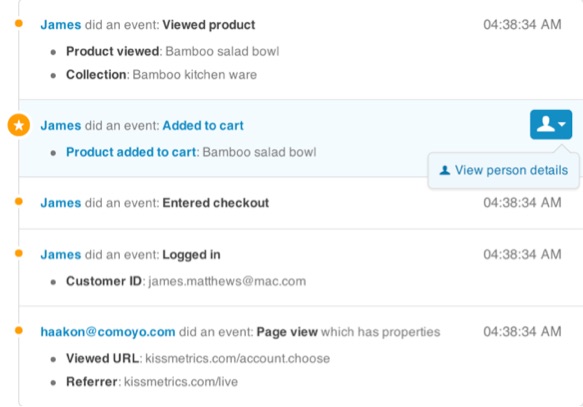

This Funnel Report will not only show you which promotional efforts are driving awareness, but also give you insight into the funnel performance for each channel, helping you identify patterns and discrepancies between how visitors from each channel (like cold vs. warm traffic) add items to your cart or complete a purchase.

You can dive even deeper into the individual customer profile, taking a look at the specific steps they took prior to purchase. This can help you identify which pages are assisting conversions, and also spot any bottlenecks or gaps that others keep hitting that causes them to bounce.

Reason #3. Make Better Marketing Decisions

Leading indicators are helpful. To a point.

They give you a preview or snapshot of what might potentially happen on down the line.

For example, SEO is a lagging indicator. Sure, you can measure new pages built and new links generated, but it's still gonna take some time for Google to reindex, new rankings to fluctuate, traffic to start dribbling, new leads converted from said traffic, and only then do you get some verifiable sales opportunities to start tracking.

That means you've got a waiting game, and in the meantime you're making a bunch of changes and assumptions based on incomplete information.

Things get especially challenging when some of these indicators can lead you astray, like when that high conversion rate might backfire.

Here's how it works: you run some headline A/B tests with generate more initial leads. Numbers go up and you pat yourself on the back. Only problem? Sales – the number that actually matters – go down as a result.

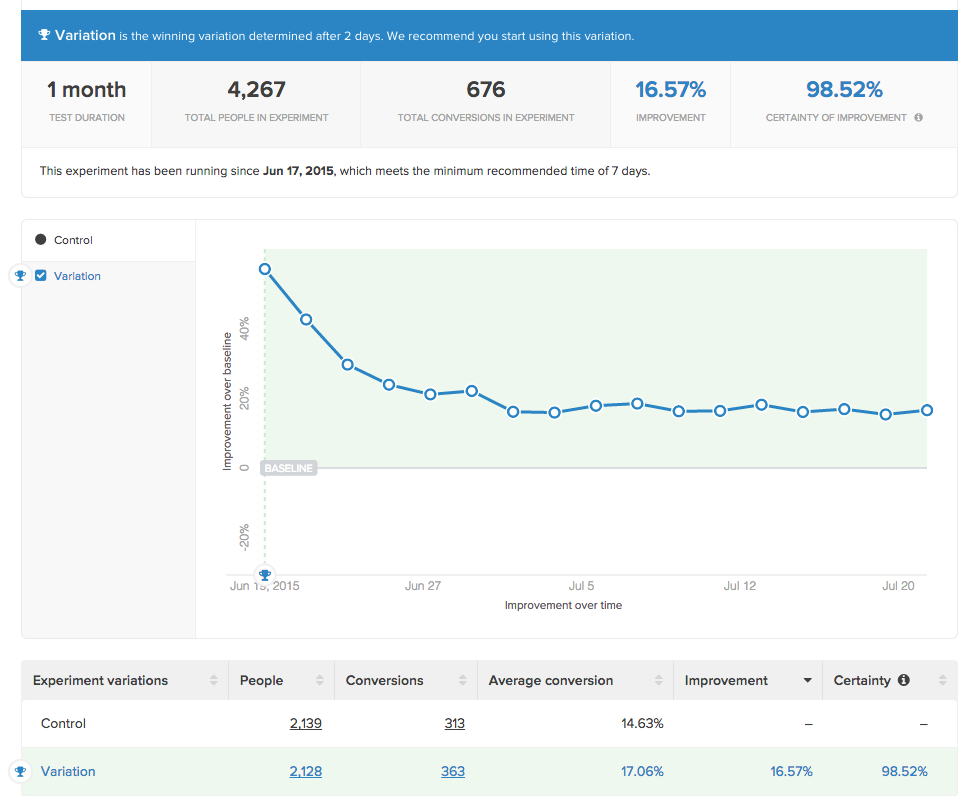

Fortunately, the Kissmetrics A/B Test Report can help you run split tests that will only declare a winner when an event is met further down the funnel, which helps you avoid getting too excited over an increase in clicks (which aren't super helpful) and waiting for the big payoff instead (conversions).

How to Sell Extra Work with Analytics Insight

Design is subjective. It shouldn't be, but it is.

My favorite thing to witness is a fiftysomething executive who has literally zero knowledge of art and design, or the owner of an old-school insurance brokerage, make specific design critiques and changes (like, “I think that shaded border should be gold instead of gray”).

Which, if I were a designer, would surely cause me to become a statistic you hear about on the Nightly News.

So how can design, something so subjective that every client thinks they can do better than your Creative Director, deliver quantifiable results that will allow you to charge more?

Look for leverage points.

For example, why does someone need that new landing page?

“I need a landing page design for an AdWords campaign,” says the client.

Ok cool – then in reality they don't just want or need one landing page, but they're gonna want (and need) multiple ones. Here's why (and how to sell it).

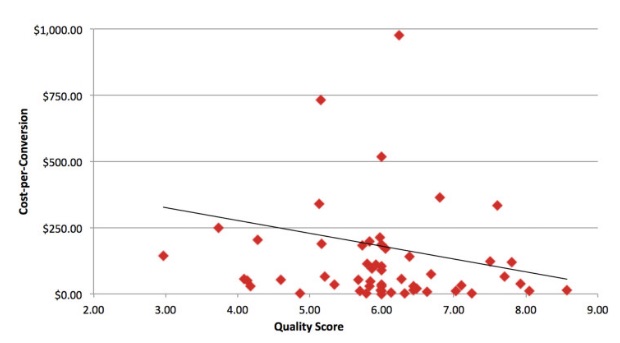

Landing page design will help dictate Quality Score, which has been proven multiple times to influence your Costs Per Click (and thus, Cost Per Conversions).

Image Source

“If your quality score increases by 1 point, your cost-per-conversion decreases by 13%,” according to Jacob from Disruptive Advertising.

Awesome. So in order to increase that quality score as much as possible, you're going to need specific and relevant landing pages for each campaign you're running. Which means you're going to need multiple versions of the same page so that you can align message match to drop your Cost Per Conversion and increase the total conversions you're getting.

Now, that's going to require some extra work.

You, dear client, will also want to make sure that copy and content changes for each page and that you set-up at least basic analytics to make sure we can track all of this and make iterations on-the-fly. That's going to require these new additional line items to our scope.

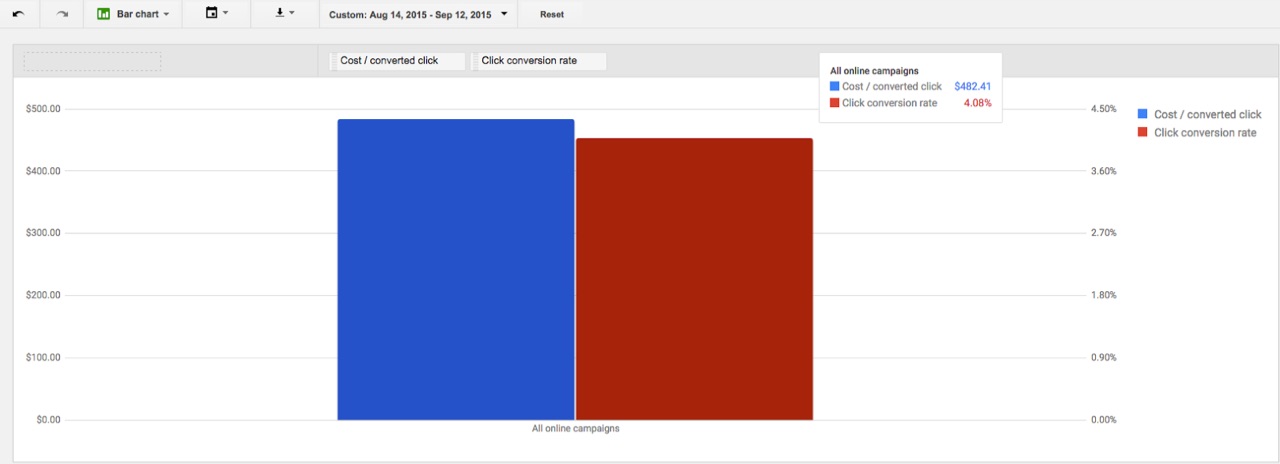

We recently went through this exact process on a new website redesign and performed a quick analysis after 30 days with the new AdWords landing pages.

The results?

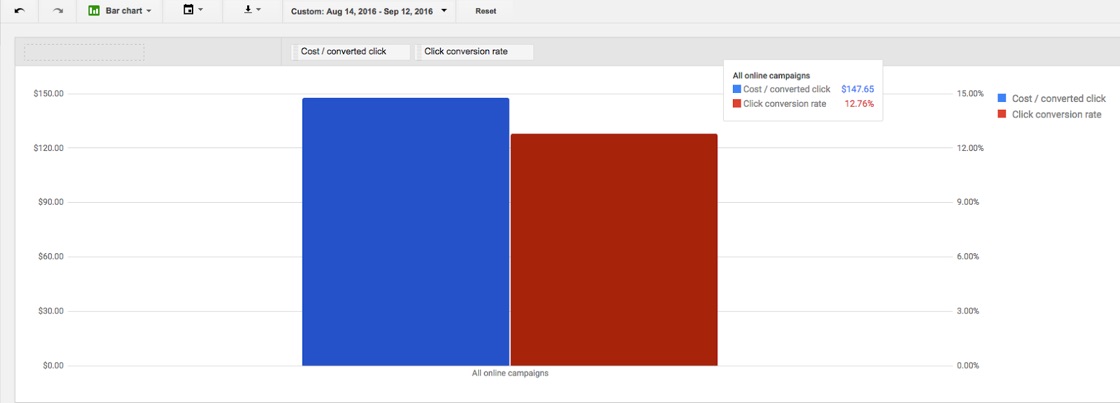

We compared results to the same period, prior year to rule out seasonality. So in 2015, their Cost Per Converted Click was $482.41 and their Conversion Rate was only 4.08%.

During the new 30-day window in 2016, their Cost Per Converted Click dropped to $147.65 and their Conversion Rate jumped to 12.76%.

Total score?

- Cost/Converted Click: 69.39% cost reduction

- Conversion Rate: 212.74% conversion rate lift

Now multiply those 'efficiency' metrics against the results (like total leads, or the amount spent for those leads), and you can quickly highlight your financial value.

Think there was enough room in that budget for a few extra landing pages? And now some more work?

Our only job as a consultant is to improve the client's position. (I think that comes from Alan Weiss.)

You're the expert, not them. And as such, you need to fight for the scope (and thus the required resources and budget) it's going to take in order to deliver the results a prospect or client is looking for (whether they understand what it's going to take or not).

Because my hairline is becoming increasingly more like Jason Statham's, and jawline has never resembled Brad Pitt's, the only way I can figure out how to do this is through cold, hard, analytical data.

Conclusion

Clients commonly don't fully understand the scope of what you're being asked to do.

That's OK. It's manageable.

But only if you can translate your value into something they do understand – like marketing KPI's or business objectives like revenue and costs.

The problem is that becomes impossible without a strong foundation for analytics.

There's no way to benchmark past performance, to isolate your individual campaigns, or spot customer bottlenecks along the way.

Fixing or addressing a client's analytics problems then should become priority #1.

Because it will not only help you justify the current work you're doing for them, but also sell the results in the future to them and new ones just like them.

About the Author: Brad Smith is a founding partner at Codeless Interactive, a digital agency specializing in creating personalized customer experiences. Brad's blog also features more marketing thoughts, opinions and the occasional insight.